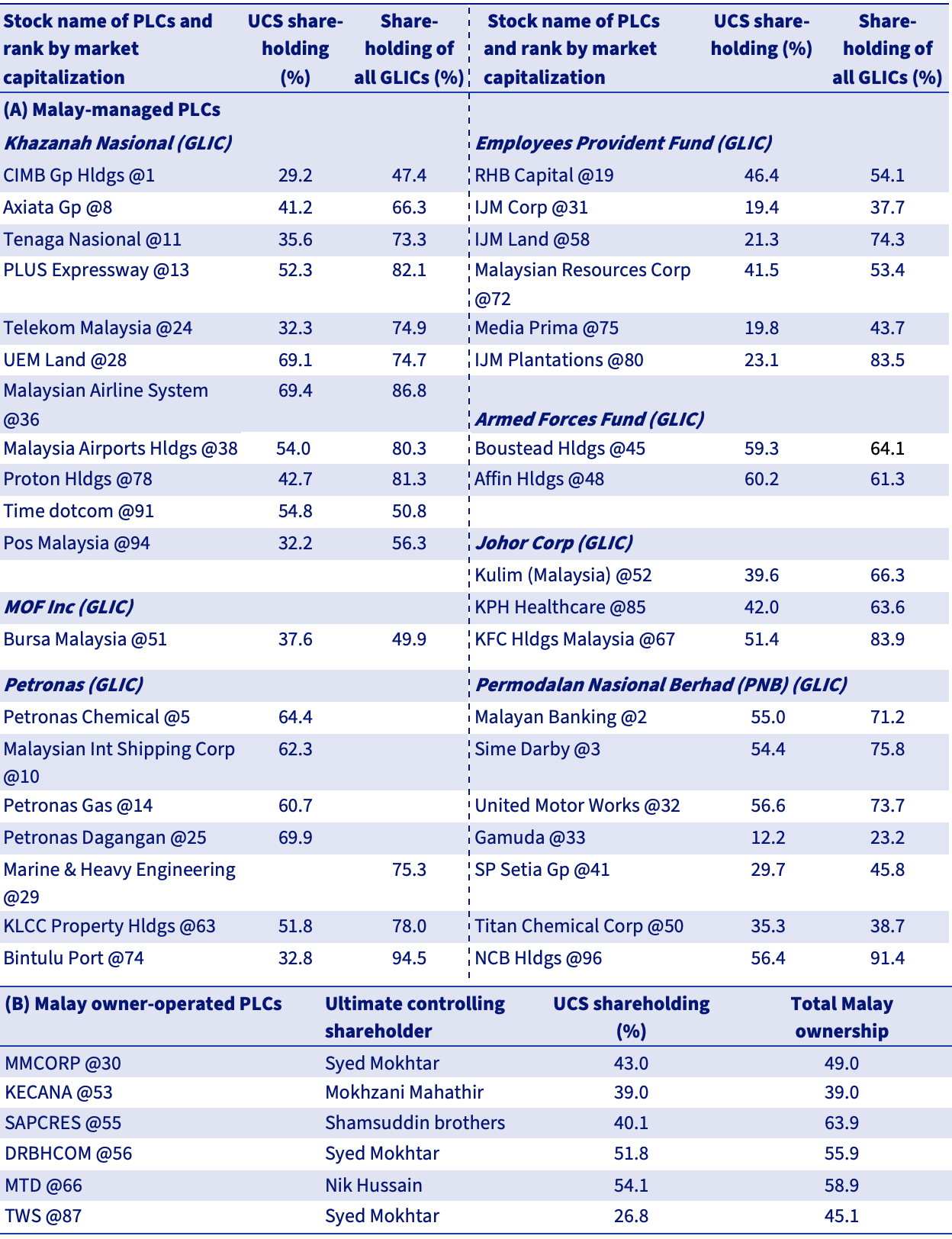

- government-linked investment companies (GLICs) or their subsidiaries, government-linked companies (GLCs); (GLICs are government-controlled and ultimately state owned or an institutional fund, such as Permodalan Nasional Berhad (PNB), established in 1978 as an implement of the NEP, and the Employees Provident Fund (EPF), set up in 1950 as a provident fund to manage a compulsory defined pension contribution plan for non-Civil Service Employees.)

- Build, lease, maintain, and transfer (BLMT) and build, lease, transfer (BLT) models—more commonly referred to as private finance initiative (PFI) models—to promote entry as an owner-manager; and

- multiple instruments to promote entry within an industry or sector.

Scaling corporate Malaysia’s heights: Corporatization and privatization

Policies, programmes, and instruments

GLICs: Opportunities and risks

In 2010, the investment of the GLICs, as a share of market capitalization, of the top 100 PLCs on Bursa Malaysia was 34.8 per cent. The total funds under management by private sector asset managers, as a share of market capitalization, was only 28.5 per cent (Securities Commission Malaysia, 2010, Table 1, pp. 6–50), equivalent to 34.9 per cent of the market capitalization of the top 100 PLCs. However, funds under private sector management include funds sourced from EPF, with some invested in other asset classes.

Funds invested by PNB, Pilgrims Fund, LTAT, and KWAP have been mobilized predominantly from Malays. Conversely, a substantial share of EPF’s retirement savings has been mobilized from non-Malays. Funding is less of an issue with KNB and Petronas. As owners and stewards of key national assets with proven cash flows and with the government’s balance-sheet support, they have less problem in accessing the debt market.

Abuse of PFI concessions

Multiple instruments to target multiple goals: Pitfalls

Promoting Malay entry into business: Owner-managers versus managers

Even to present, failures have not necessarily been caused by the ownership structure of the enterprise. Constraints have often arisen in the financing of the investment and sale. For example, with water-treatment plants and water distribution, pricing and underinvestment were serious issues. The water distributor was able to sell to end consumers at the controlled price so long as it did not have to overpay for its treated water. The most serious problems arose when the two lines of business were operated as separate businesses, rather than on a combined basis where they were able to generate a small operating surplus, irrespective of ownership, as in Penang, which was state owned, and in Johor, which was privately owned (Pua, 2011; Tan, 2012).

Concluding remarks

Berle, A. A. and Means, G. C. 1932. The Modern Corporation and Private Property. New York: Harcourt, Brace and World, Inc.

Gomez, E. T. Padmanabhan, T. Norfaryanti Kamaruddin, and Bhalla, S. 2017. Minister of Finance Incorporated, Ownership and Control of Corporate Malaysia. Singapore: Palgrave Macmillan.

Hassan, B. W. 2012. ‘Ownership and Control of Public Listed Companies in Malaysia: The Impact of the New Economic Policy’. MSc Dissertation. University of Malaya.

La Porta, R. Lopez-de-Silanes, F. Shleifer, A. and Vishny, R. W. 1998. ‘Law and Finance’, Journal of Political Economy, 106/6, pp. 1113–1155.

Ministry of Finance, Malaysia. 2023. Economic and Fiscal Outlook and Federal Government Revenue Estimates 2023. Kuala Lumpur: Government Printing Press.

Pua, T. 2011. The Tiger that Lost its Roar: A Tale of Malaysia's Political Economy. Kuala Lumpur: Democratic Action Party.

Rajasingam, M. 2020. Navigating Turbulent Times: The Memoirs of M. Rajasingam. Petaling Jaya: Strategic Information and Research Development Centre.

Securities Commission Malaysia. 2010. Annual Report. Kuala Lumpur: Securities Commission.

Segawa, N. Natsuda, K. and Thoburn, J. 2014. ‘Affirmative Action and Economic Liberalization: The Dilemmas of the Malaysian Automotive Industry’. Asian Studies Review, June, pp. 422–441.

Tan, J. 2008. Privatization in Malaysia: Regulation, Rent-seeking and Policy Failure. New York: Routledge.

______ 2012. ‘The Pitfalls of Water Privatisation: Failure and Reform in Malaysia’. World Development, 40/12, December, pp. 2552–2563.

______ 2015. ‘Water Privatization, Ethnicity and Rent-Seeking Preliminary Evidence from Malaysia’. Journal of Southeast Asian Economies, 32/ 3, pp. 297–318.

Tate, D. J. M. 1989. Power Builds the Nation: the National Electricity Board of the States of Malaya and its Predecessors. Volume 1: The Formative Years. Kuala Lumpur: National Electricity Board of the States of Malaya.

______ 1990. Power Builds the Nation: the National Electricity Board of the States of Malaya and its Predecessors. Volume 2: Transition and Fulfilment. Kuala Lumpur: National Electricity Board of the States of Malaya.

Thillainathan, R. 2021. ‘Privatisation of Toll Roads to Promote Malay Entry into Business in Malaysia: A Critical Review of Distribution Stance, Returns, Risk and Governance’. Malaysian Journal of Economic Studies, 58/1, pp. 145–174.

______ 2022. ‘Privatisation of Power Generation in Malaysia: Impact on the Entry of Malays into Power Business’. Malaysian Journal of Economic Studies, 59/1, pp. 71–91.

______ 2024. Early Post-Independence Malay Entry into Business: Achievements and Failures. https://www.ehm.my/publications/articles/early-post-independence-malay-entry-into-business-achievements-and-failures

Thillainathan, R. and Cheong, K. C. 2016. ‘Malaysia’s New Economic Policy, Growth and Distribution: Revisiting the Debate’. Malaysian Journal of Economic Studies, 53/1, pp. 51–68.

______ 2019. ‘Malaysian Public-Private Partnerships: Incentivising Private Sector Participation or Facilitating Rent-Seeking?’. Malaysian Journal of Economic Studies, 56/2, pp. 177–200.

______ 2024. ‘Malay Entry into Business through Scaling the Heights of Corporate Malaysia from mid-1980s—An Assessment’. Malaysian Journal of Economic Studies, 61/2, pp. 265–289.

Vithiatharan, V. and Gomez, E. T. 2014 ‘Politics, Economic Crises, and Corporate Governance Reforms: Regulatory Capture in Malaysia’. Journal of Contemporary Asia, 44/4, pp. 599–615.

Wain, B. 2012. Malaysian Maverick: Mahathir Mohamad in Turbulent Times. 2nd Edition. Hampshire: Palgrave Macmillan.

Wong, S. 2011. Notes to the Prime Minister: The Untold Story of How Malaysia Beat the Currency Speculators. Petaling Jaya: MPH Group Publishing.