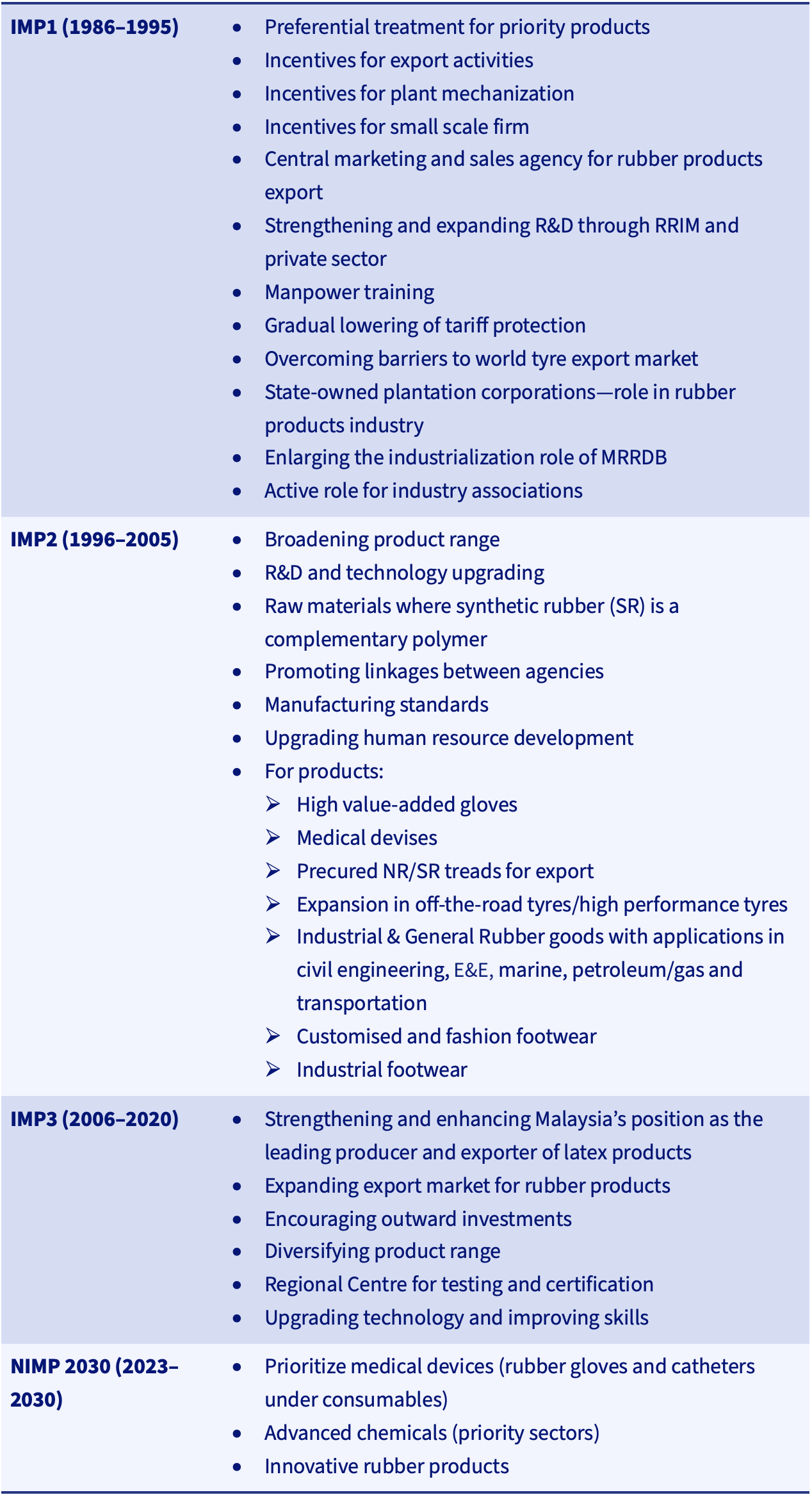

Industrial Master Plans, 1986–2030

Policies

Institutional Support

Several key rubber research institutions have helped the rubber industry in its upstream development, notably, the Rubber Research Institute of Malaysia (RRIM), which was established by the colonial government in 1925 to improve methods of cultivation, pest control, processing, as well as yields, given that rubber was an important export commodity for the British Empire (Kawano, 2019). After independence, the RRIM continued to develop high-yield varieties and to encourage their use in replanting. Importantly, the RRIM laid a solid foundation for the development of natural rubber, which became the basis for the venture into rubber products manufacturing.

The Malaysian Rubber Research Development Board (MRRDB) was subsequently established to oversee the research, technical development, and promotional work of the Malaysian rubber industry. MRRDB has two research institutions under its wings, namely RRIM and the Tun Abdul Razak Research Centre. The latter focuses on research for practical uses of rubber, including on research on advanced materials, upscale rubber products, engineering processes, and biotechnology. MRRDB is thus able to provide technical support for domestic manufacturers through its research institutes and technical advisory service units.

Later, in 1998, the Malaysian Rubber Board (MRB) was established by the merger of the three key agencies responsible for Malaysia's rubber industry, namely the RRIM, MRRDB, and the Malaysian Rubber Exchange and Licensing Board (MRELB). The MRB operates as an agency under the Ministry of Primary Industries. It is crucial in enhancing the capability of the rubber industry through research and development, technical and non-technical support services, and regulatory functions, through the issuance of licences and permits, which encompass the upstream (production), midstream (processing), and downstream (manufacturing) sectors. MRB also reviews and recommends to government improvements related policies, regulations, and procedures.

The MRB has a product certification system for rubber quality assurance. For example, the MRB Product Certification Mark is granted to rubber product manufacturers that meets its requirements. In keeping with the shift towards sustainability, the MRB is developing the Malaysian Sustainable Natural Rubber (MSNR) standard, through which the MSNR will be awarded to MRB licence and permit holders that meet the MSNR’s five principles: no deforestation for rubber planting, rubber planting in accordance with the National Land Code, environmental sustainability, social compliance, and supply chain traceability (Bernama, n.d.). MSNR enforcement is set to begin on 1 January 2025, and MRB licence and permit holders must comply with its standard operating procedures to obtain MSNR certification.

Two types of cesses are collected to fund the MRB. The first is a tax on rubber exports, imposed since 1907. Nearly a century later, a cess of 0.2 per cent on the export of rubber products was also imposed by the Malaysian Rubber Board in 1999. Some 80 per cent of this second cess is used to support the programmes and activities of the Malaysian Rubber Council (MRC), established in 2000, as a company limited by guarantee under the Ministry of Plantation and Commodities, for the promotion and marketing of Malaysian rubber and rubber products on global markets. The MRC maintains offices in the United States, China, and India, indicating the critical importance of rubber exports as Malaysia already has a national trade promotion agency, MATRADE, under the Ministry of Investment, Trade and Industry (MITI). MATRADE was established in 1993 and modelled after JETRO in Japan.

Trade associations have been active since they were involved as key stakeholders delivering outputs related to IMP1. Thus, the Malaysian Rubber Products Manufacturers’ Association (MRPMA), Malaysian Rubber Glove Manufacturers Association (MARGMA), Malaysian Rubber Processors Association (MRPA), and Association of Malaysian Medical Industries (AMMI) are all part of the Board of Trustees of MRC, besides other representatives from the relevant ministries.

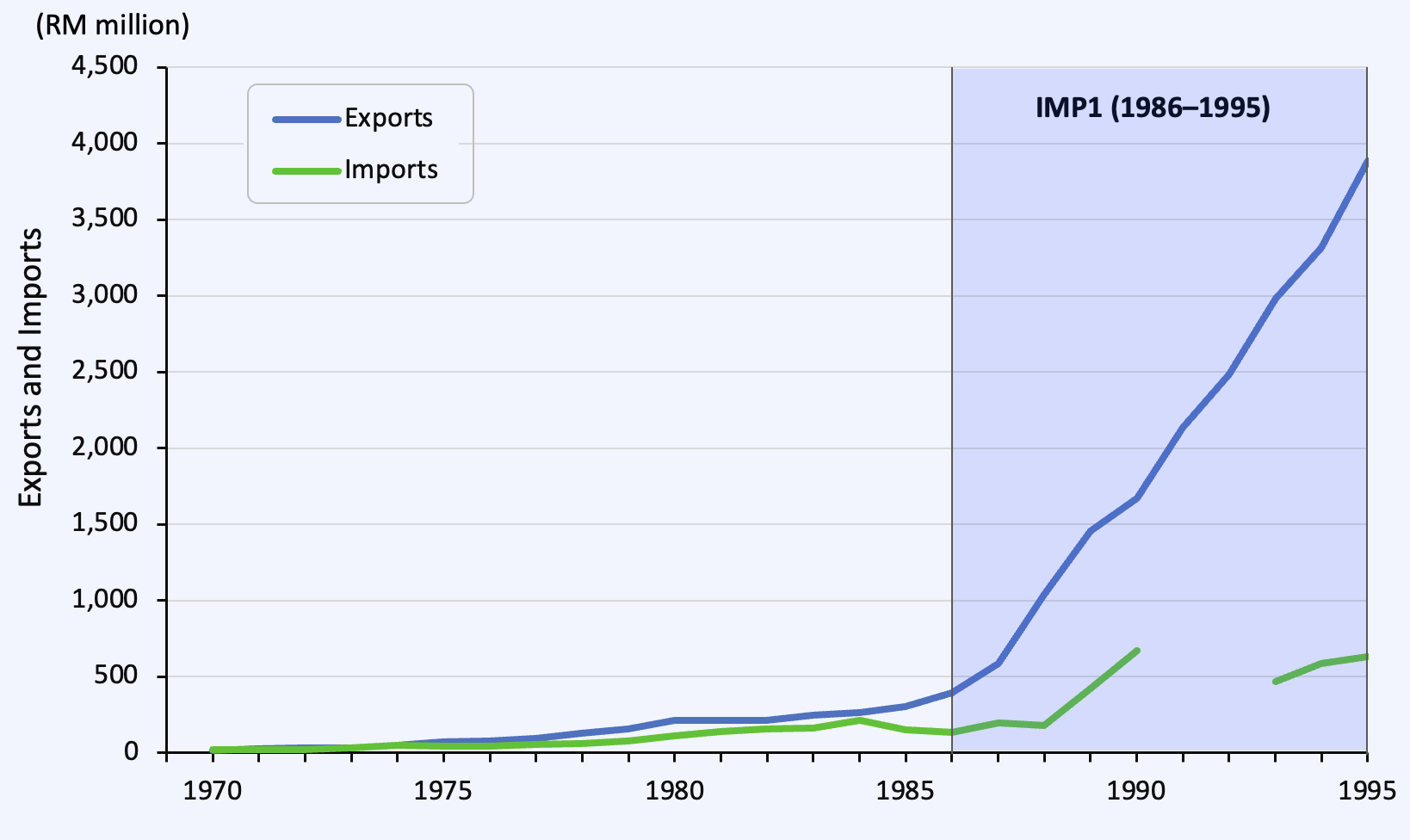

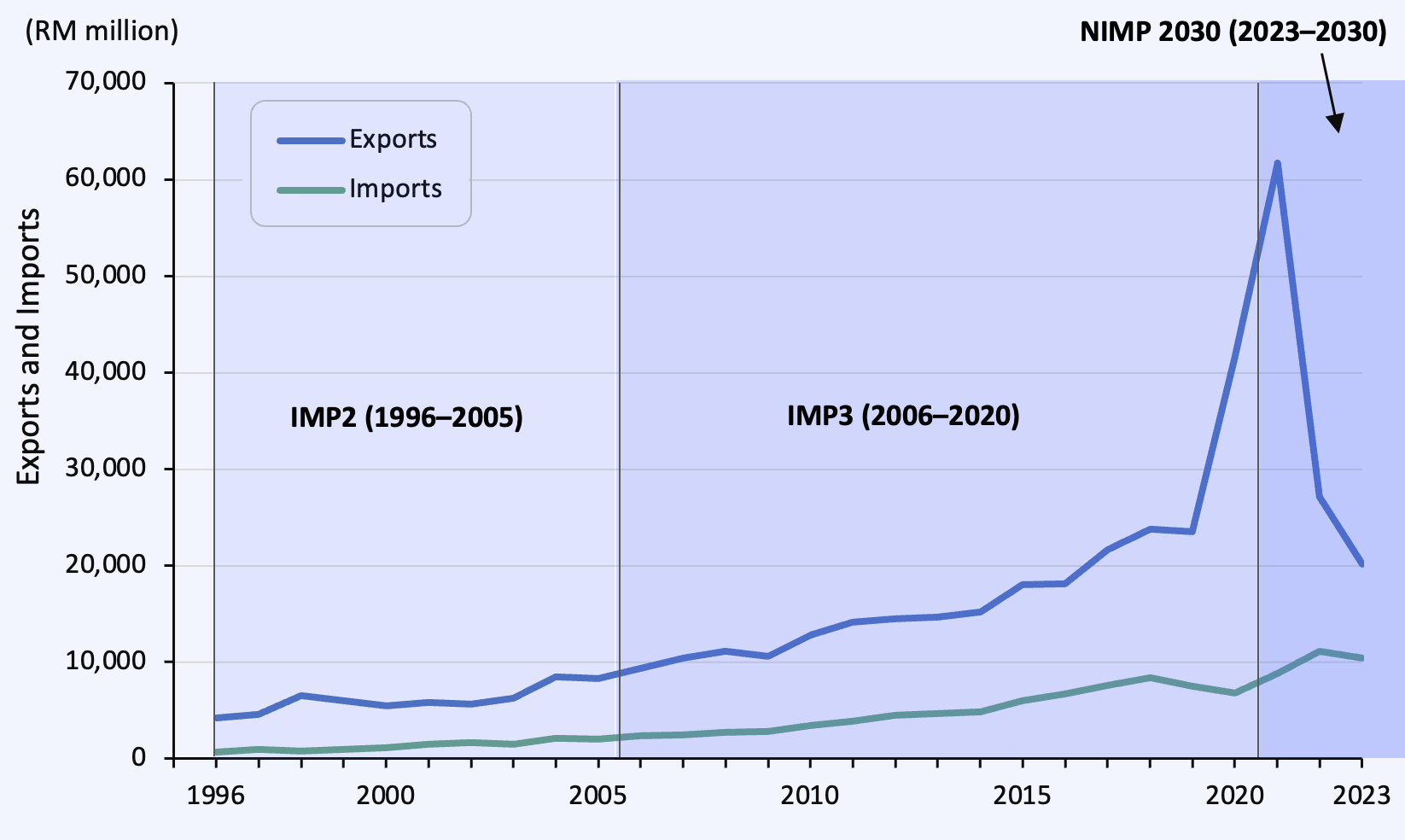

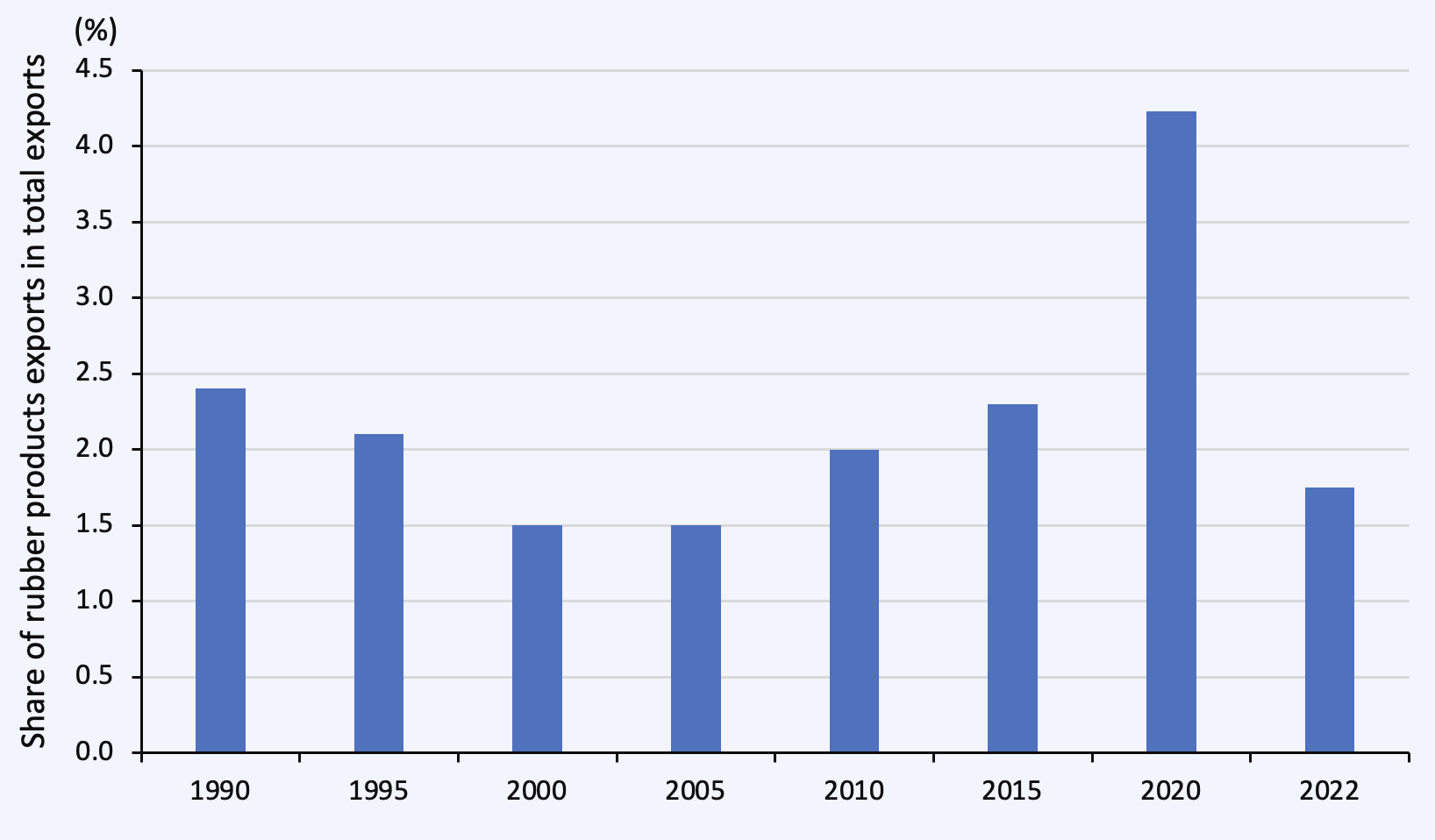

Performance of the Rubber Products Sector

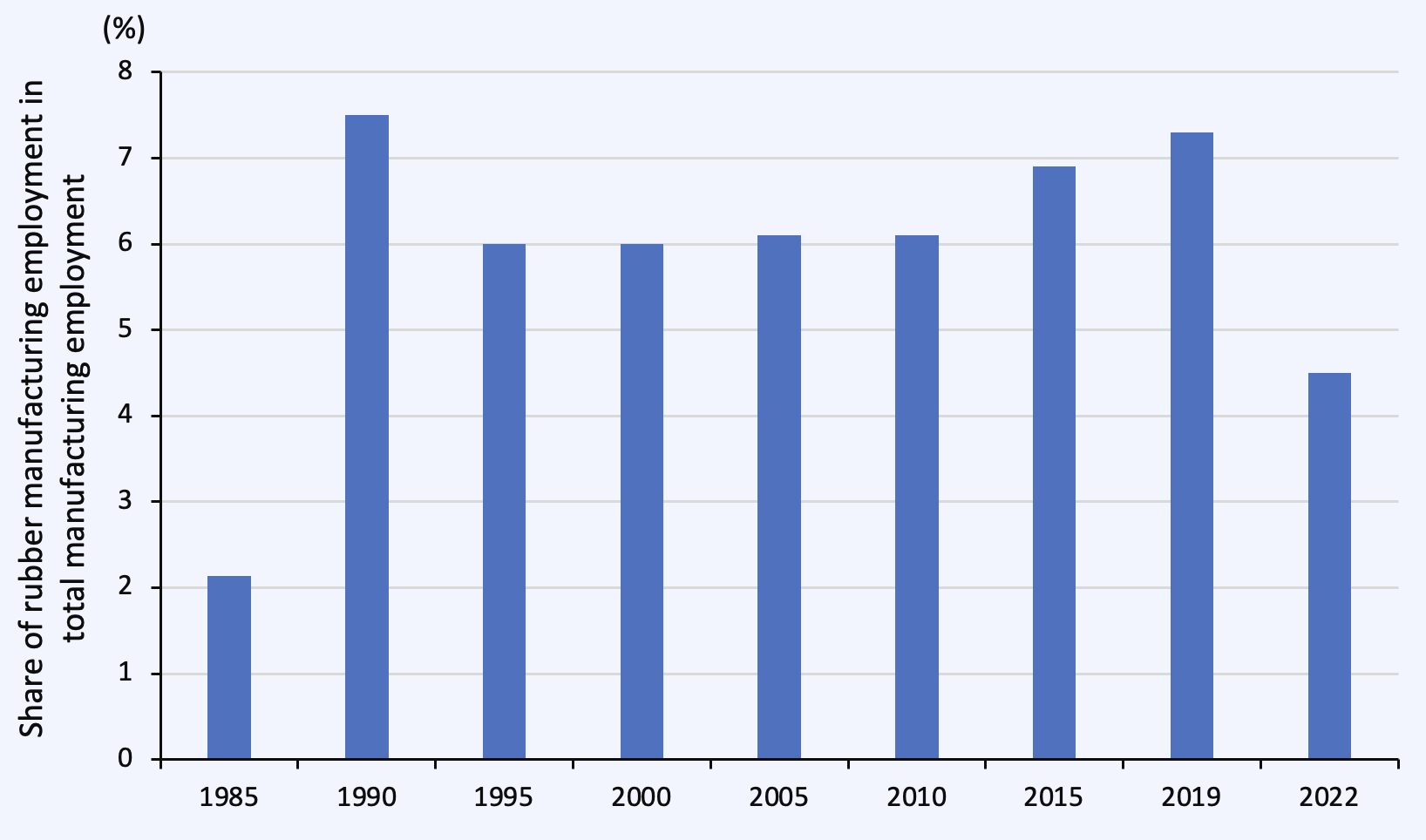

International Trade and Employment

Consumption of Natural Rubber

Kedah Rubber City

Challenges in Moving Forward

Dualistic Manufacturing Sector

ESG Compliance

Research and Innovation

Conclusion

Ahmad Farouk Haji S. M. Ishak, 1992. ‘Development of the Rubber-based Industries: The Malaysian Experience.’ Public Affairs Series, PAS12/92. Kuala Lumpur: Malaysian Rubber Research and Development Board (MRRDB).

Athukorala, P. C. and Narayanan, S. 2017. ‘Economic Corridors and Regional Development: The Malaysian Experience.’ ADB Economics Working Paper Series No. 520, 2–17 December. https://www.adb.org/sites/default/files/publication/411956/ewp-520-malaysia-economic-corridors-regional-development.pdf . Accessed 13 November, 2024.

Bernama. 2024. ‘MSNR Agenda Boosts National Rubber Industry, Empowers Smallholders.’ https://www.bernama.com/en/bfokus/news.php?id=2347730. Accessed 13 November 2024.

Fadillah, Y. 1991. ‘The Rubber Products Industry–Towards 2020.’ Malaysia Rubber Producer Manufacturing Association (MRPMA). 1992/93 Rubber Products & Export Directory. Subang Jaya: MRPMA.

Federation of Malaysian Manufacturers (FMM). (n.d.). ‘Country Report for Petrochemical: Synthetic Rubber.’ (https://www.fmm.org.my/upload/Country_Report_for_Petrochemical-Synthethic_Rubber.pdf. Accessed 13 November 2024.

Goldthorpe, C. C. 2009. ‘Resource-based Industrialization in Peninsular Malaysia: A Case Study of the Rubber Products Manufacturing Industry.’ Unpublished PhD thesis, University of Bradford. https://core.ac.uk/download/pdf/136777.pdf. Accessed 13 November 2024.

______ 2015. Rubber Manufacturing in Malaysia: Resource-based Industrialization in Practice. Singapore: NUS Press.

Hutchinson, F. and Bhattacharya, P. 2021. ‘Malaysia’s Rubber Glove Industry – The Good, the Bad and the Ugly.’ Perspective 2021/35. Singapore: ISEAS-Yusof Ishak Institute.

International Bank for Reconstruction and Development (IBRD). 1955. The Economic Development of Malaya: Report of a Mission Organized by the IBRD at the request of the Federation of Malaya, the Crown Colony of Singapore and the United Kingdom. Washington, DC: IBRD.

International Labour Organization (ILO). 2024. ‘Special podcast episode: Malaysia’s rubber industry takes on forced labour.’ https://flbusiness.network/new-podcast-tackling-forced-labour-malaysia-rubber-industry/ Accessed 19 November 2024 .

Kawano, M. 2019. ‘Changing Resource-Based Manufacturing Industry: The Case of the Rubber Industry in Malaysia and Thailand.’ In: Tsunekawa, K., and Todo, Y. (eds) Emerging States at Crossroads. Emerging-Economy State and International Policy Studies. Singapore: Springer. https://doi.org/10.1007/978-981-13-2859-6_7.

Lee, S. M., Radziah Adam, and Ku’ Azam, T. L. 2020. ‘The Effects of Tax and Promotion on Rubber Medical Devices Export.’ Jurnal Ekonomi Malaysia, 54(2), pp. 29–40.

Lee, L., Mazlina Abdul Rahman, and Syed Mohamad Bukhari Syed Bakeri. 2024. ‘Industry Focus: Rubber Products’. Kuala Lumpur: SME Bank. https://www.smebank.com.my/documents/d/guest/RubberProducts_Feb2024. Accessed 13 November 2024.

Lim, C. Y. 1967. Economic Development of Modern Malaya. Kuala Lumpur: Oxford University Press

Lim, S. C. 1985. ‘Industrialization: Role and Prospects of the Malaysian Rubber-Based Industry.’ MRRDB Monograph No. 11. Petaling Jaya: Malaysian Rubber Research and Development Board (MRRDB).

______ 1991. Rubber Products Industry: Are We on Course? Petaling Jaya: Malaysia Rubber Producer Manufacturing Association (MRPMA).

Malaysian Rubber Council (MRC). 2024. ‘Malaysian Rubber Council Leads Sustainability Drive in Rubber Industry.’ (Press Release by Malaysian Rubber Council on 18 January 2024)https://www.dpworld.com/-/media/project/dpwg/dpwg-tenant/corporate/global/media-files/all-insights/expert-opinion/malaysian-rubber-councils-green-rubber.pdf?rev=3369009eaaca49e997bfabdd7acb5072&hash=AA4B7CA84632DCC48E10E74127C187B2. Accessed 13 November 2024.

Malaysian Investment Development Authority (MIDA) (n.d.). Rubber Products https://www.mida.gov.my/industries/manufacturing/chemical-advanced-materials/chemicals-advance-materials-rubber-products/. Accessed 13 November 2024.

Ministry of International Trade and Industry–Malaysia (MITI). First Industrial Master Plan, 1986–1995 (IMP1). Kuala Lumpur: MITI.

______ 1996. Second Industrial Master Plan, 1996–2005 (IMP2). Kuala Lumpur: MITI.

______ 2006. Third Industrial Master Plan, 2006–2020 (IMP3). Kuala Lumpur: MITI.

Ministry of Investment, Trade and Industry (MITI). 2023a. New Industrial Master Plan 2030. Kuala Lumpur: MITI.https://www.nimp2030.gov.my/. Accessed 13 November 2024.

______ 2023b. New Industrial Master Plan 2023: Rubber-Based Products Industry. Kuala Lumpur: MITI. https://www.nimp2030.gov.my/nimp2030/modules_resources/bookshelf/e-18-Sectoral_NIMP-Rubber-based_Products_Industry/e-18-Sectoral_NIMP-Rubber-based_Products_Industry.pdf. Accessed 13 November 2024.

Northern Corridor Economic Region (NCER), Kedah Rubber City. https://www.ncer.com.my/invest-in-ncer/thematic-industrial-parks/kedah-rubber-city-krc. Accessed 23 November 2024.

Sultan Nazrin Shah. 2019. Striving for Inclusive Development: From Pangkor to a Modern Malaysian State. Kuala Lumpur: Oxford University Press.

Tham, S. Y. 2007. ‘Outward Foreign Direct Investment from Malaysia: An Exploratory Study.’ Journal of Current Southeast Asian Affairs. 26/5, pp. 44–72.

The Edge. 2021. ‘Glove Manufacturers Repurpose ESG Compliance into Healthcare.’ 1 December issue. https://theedgemalaysia.com/content/advertise/glove-manufacturers-repurpose-esg-compliance-healthcare. Accessed 13 November 2024.

______ 2024. ‘Hong Seng Revisits Potential Glove Business Expansion, but on Smaller Scale.’ 21 May issue.https://theedgemalaysia.com/node/712539. Accessed 13 November 2024.Top Glove Corporation Bhd. (n.d.). “Innovation.” https://www.topglove.com/innovation. Accessed 13 November 2024.

World Integrated Trade Solution (WITS). 2023. ‘Gloves (401511) Exports by Country in 2023.’ https://wits.worldbank.org/trade/comtrade/en/country/ALL/year/2023/tradeflow/Exports/partner/WLD/nomen/h5/product/401511. Accessed 13 November 2024.

World Wide Fund Malaysia (WWF–M). 2021. Mapping the Natural Rubber Value Chain in Malaysia. https://wwfmy.awsassets.panda.org/downloads/mapping_natural_rubber_6_april_2022.pdf. Accessed 13 November 2024.