Malaya was much more prosperous than most territories in the British Empire, and returns on investment in Malaya were among the Empire’s highest by the 1930s (Rönnbäck et al., 2022). Benchmark gross domestic product (GDP) figures show real per capita income growth of 4.1 per cent annually between 1900 and 1929, more than double the rate of Japan. In 1929, per capita GDP in Malaya (excluding Singapore) was US$1,910, compared with US$1,191 in Japan (Huff, 2002, p. 1,077; Maddison, 1995, pp. 94–97). Between 1910 and 1939, real private final consumption expenditure in Malaya increased from Straits$206 million to Straits$518 million (at constant 1914 prices) (Sultan Nazrin Shah, 2017, appendix 2). However, economic prosperity was not accompanied by a shift in the economic structure towards manufacturing to meet the expanding domestic demand.

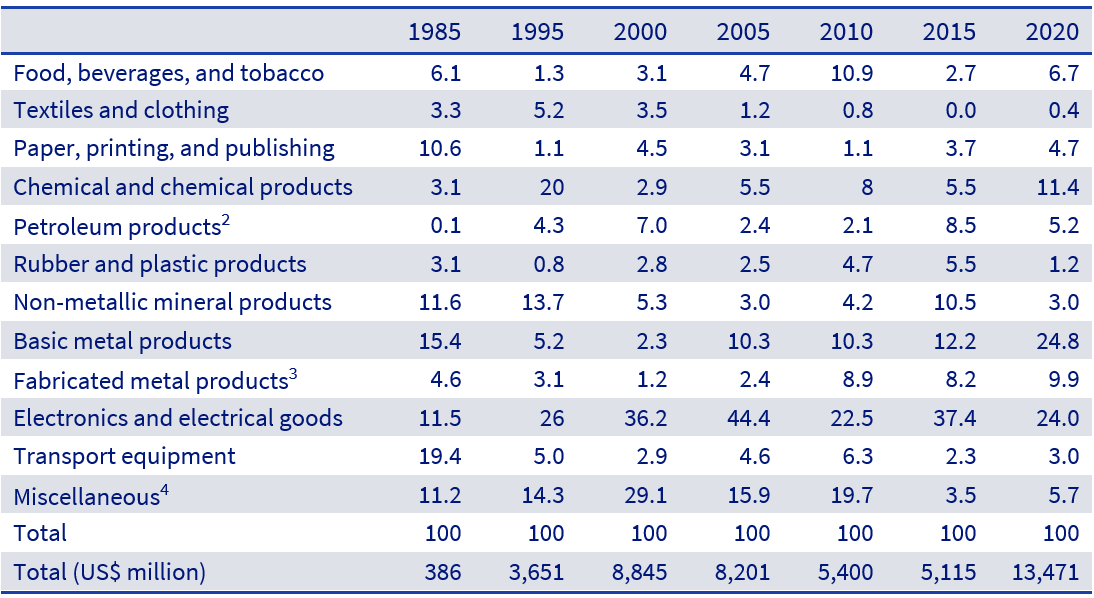

Malaya's manufacturing sector employed just 7.1 per cent of workers in 1921, a share that had increased to only 9.8 per cent in 1947 (Huff, 2002, table 3). Even in 1961, the earliest year for which sectoral GDP estimates are available, manufacturing accounted for only 6 per cent of GDP (Wheelwright, 1965). Nearly half of manufacturing was accounted for by factory processing of primary products—that is, rubber processing and tin smelting. Within ‘secondary manufacturing’4 , organized factory production was largely linked to the primary sector—mainly production of machinery for rubber and tin industries and a range of ‘non-tradable’ manufactures5 such as building material, furniture, and aerated water for the modern sector of the economy, which all evolved around the plantation sector and tin mining (Allen and Donnithorne, 2013; Thorburn, 1977; White, 1999).

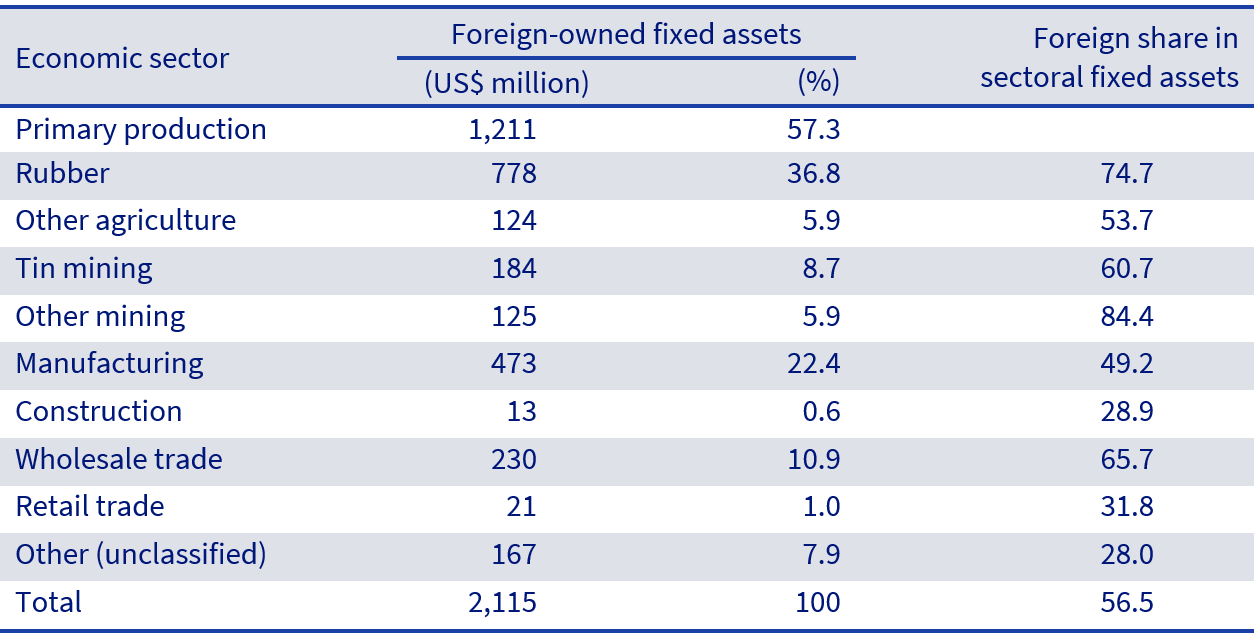

Primary processing and ‘organized’ secondary manufacturing was predominantly, if not solely, the preserve of Western firms. The rest of secondary manufacturing comprised small-scale and cottage production of food and handicrafts undertaken predominantly by Chinese and to a lesser extent Indians entirely for the domestic market (IBRD, 1955). There was no incentive for foreign investors to engage in manufacturing to meet domestic demand, given the colonial free trade regime that assured ready availability of imports at world prices.

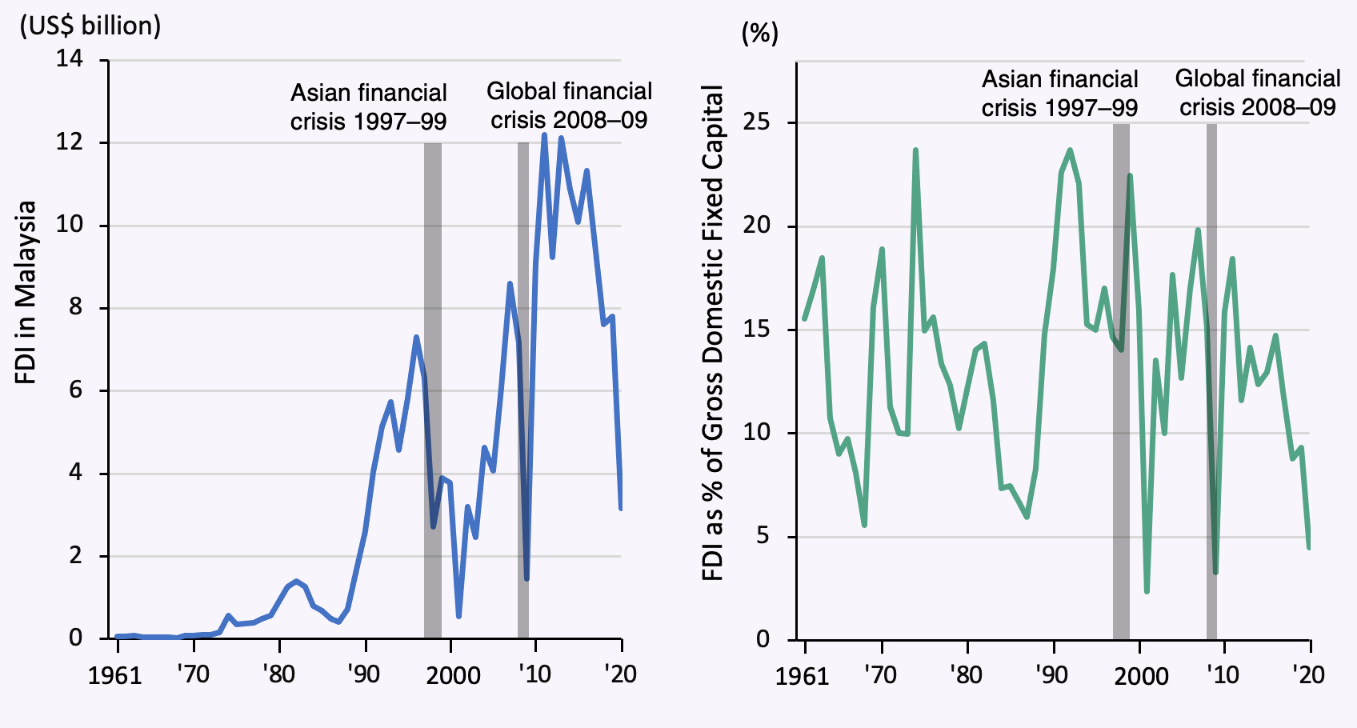

Impact of Financial Crises: Regional comparisons

What explains Malaysia's recent sharp decline in FDI?

Dualistic incentive structure

Skill and innovation deficits

Allen, G. C. and A. G. Donnithorne, A. G. 2013. Western Enterprises in Indonesia and Malaya. Reprint. London: Routledge.

Athukorala, P. 2001. Crisis and Recovery in Malaysia: The Role of Capital Controls. Cheltenham: Edward Elgar Publishing.

______ 2003. ‘Foreign Direct Investment in Crisis and Recovery: Lessons from the 1997–1998 Asian Crisis’. Australian Economic History Review, 43(2), pp. 197–213.

______ 2007. Multinational Enterprises in Asian Development. Cheltenham: Edward Elgar Publishing.

______ 2011. ‘The Malaysian Economy During Three Crises’ in Hill, H., Tham, S-Y, and Ragayah, Haji M. Z. (eds.), Graduating from the Middle: Malaysia’s Development.

______ 2014. ‘Growing with Global Production Sharing: The Tale of Penang Export Hub, Malaysia’. Competition and Change, 18(3), pp. 221–245.

Athukorala, P. and Kohpaiboon, A. 2015. 'Global production sharing, trade patterns, and industrialization in Southeast Asia', in Coxhead, I. A. (ed.), Routledge handbook of Southeast Asian Economics. London and New York: Routledge, pp. 139–61.

Bank Negara Malaysia (BNM) (1994). Money and Banking in Malaysia, 35th Anniversary Edition, 1959–1994, Kuala Lumpur: BNM.

Barlow, C. 1978. The Natural Rubber Industry: Its Development, Technology, and Economy in Malaysia. Kuala Lumpur: Oxford University Press.

Brockway, L. H. 1979. ‘Science and Colonial Expansion: The Role of The British Royal Botanic Gardens’. American Ethnologist, 6(3), pp. 449–465.

Callis, H. G. 1942. Foreign Capital in Southeast Asia. New York: Institute of Pacific Relations.

Chia, S. Y. 2011. ‘Inward and Outward FDI and the Reconstructing of the Singapore Economy’ in Susangkarn, C., Young, C. P., and Sung, J. K. (eds.), Foreign Direct Investment in Asia. London: Routledge, pp. 121–176.

Christopher, A. J. 1985. ‘Patterns of British Overseas Investment in Land, 1885–1913’. Transactions of the Institute of British Geographers, 10(4), pp. 452–466.

Department of Statistics–Malaysia. 1968. Report on the Financial Survey of Limited Companies 1968. Kuala Lumpur: Department of Statistics.

Drabble, J. H. and Drake, P. J. 1981. ‘The British Agency Houses in Malaysia: Survival in a Changing World’. Journal of Southeast Asian Studies, 12(2), pp. 297–328.

Drake, P. J. 1979. ‘The Economic Development of British Malaya to 1914: An Essay in Historiography with Some Questions for Historians’. Journal of Southeast Asian Studies, 10(2), pp. 262–290.

Faaland, J., Parkinson, J. R., and Rais, B. S. 1990. Growth and Ethnic Inequality: Malaysia's New Economic Policy (NEP). Kuala Lumpur: Dewan Bahasa dan Pustaka.

Gomez, E. T. 2011. ‘The Politics and Policies of Corporate Development: Race, Rents and Redistribution in Hill, H., Tham, S-Y., and Ragayah, Haji M. Z. (eds.), Graduating from the Middle: Malaysia’s Development.

Huff, W. G. 2002. ‘Boom-or-Bust Commodities and Industrialization in Pre–World War II Malaya’. The Journal of Economic History, 62(4), pp. 1074–1115.

International Bank for Reconstruction and Development (IBRD). 1955. The Economic Development of Malaysia. Baltimore: Johns Hopkins University Press.

Jesudasan, J. V. 1989. Ethnicity and the Economy: The State, Chinese Business, and Multinationals in Malaysia. Singapore: Oxford University Press.

Jomo, S. K. 2004. ‘Afterword’ in Puthucheary, J. J., Ownership and Control in the Malaysian Economy: A Study of the Structure of Ownership and Control and its Effects on the Development of Secondary Industries and Economic Growth in Malaya and Singapore. Selangor Darul Ehsan: INSAN.

Kamariah-Ghazali, S. 2021. The Real Exchange Rate and Economic Performance: Insights from the Malaysian Experience. PhD Thesis. Canberra: Australian National University. https://openresearch-repository.anu.edu.au/handle/1885/267264

Lim, D. 1992. ‘The Dynamics of Economic Policy-making: A Study of Malaysian Trade Policies and Performance’, in Maclntyre, A. J. and Kanishka, J. (eds.), The Dynamics of Economic Policy Reforms in South-east Asia and the South-west Pacific. Singapore: Oxford University Press, pp. 94–114.

Lindblad, J. T. 1998. Foreign Direct Investment in Southeast Asia in the Twentieth Century. London: Macmillan.

Maddison, A. 1995. Monitoring the World Economy 1820–1992. Paris: OECD.

Menon, J. and Ng, T. H. 2013. ‘Are Government-linked Companies Crowding out Private Investment in Malaysia?’. ADB Economics Working Papers, No. 345, Manila: Asian Development Bank.

Ong, W. L. 2022. Solving the Skills Crunch: Penang Industries Face Hiring Challenges during Economic Recovery. Penang Institute Monograph. George Town: Penang Institute. https://penanginstitute.org/wp-content/uploads/2022/08/Solving-the-skills-crunch.pdf.

Rasiah, R. 1995. Foreign Capital and Industrialisation in Malaysia. London: Macmillan.

Rönnbäck, K., Broberg, O., and Galli, S. 2022. ‘A Colonial Cash Cow: The Return on Investments in British Malaya, 1889–1969’. Cliometrica, 16(1), pp. 149–173.

Sachs, J. and Warner, A. 1995. ‘Economic Reforms and the Process of Global Integration’. Brooking Papers on Economic Activity, 1, pp. 1–118.

Saham, J. 1980. British Industrial Investment in Malaysia, 1963–1971. Kuala Lumpur: Oxford University Press.

Socio-Economic Research Institute (SERI). 2008. Penang Industrial Survey 2007. Penang: SERI.

Sultan Nazrin Shah. 2017. Charting the Economy: Early 20th Century Malaya and Contemporary Malaysian Contrasts. Kuala Lumpur: Oxford University Press.

______ 2019. Striving for Inclusive Development: From Pangkor to a Modern Malaysian State. Kuala Lumpur: Oxford University Press.

Singh, C. 2011. ‘The PDC as I know It (1970–1990)’, in Malaysia: Policies and Issues in Economic Development. Kuala Lumpur: Institute of Strategic International Studies, pp. 597–622.

Thorburn, J. T. 1977. Primary Commodity Exports and Economic Development: Theory, Evidence and a Study of Malaysia. London: Wiley.

United Nations Conference on Trade and Development (UNCTAD). 2005. World Investment Report. Geneva: UNCTAD.

Warr, P. 1987. ‘Malaysia’s Industrial Enclaves: Benefits and Costs’. The Developing Economies, 25(1), pp. 30–55.

Winstedt, R. 1966. Malaya and Its History. 7th ed. London: Hutchinson University Library.

Wheelwright, E. L. 1965. Industrialization in Malaysia. Melbourne: Melbourne University Press.

White, N. J. 1999. ‘Gentlemanly Capitalism and Empire in the Twentieth Century: The Forgotten Case of Malaya, 1914–1965’, in Dumett, R. E. (ed.), Gentlemanly Capitalism and British Imperialism: The New Debate on Empire. London: Routledge, pp. 175–195.

World Bank. 2022. Malaysia Economic Monitor Report. Kuala Lumpur: World Bank.

Install EHM PWA App