The pre-NEP era (1957–1970): Emergence of Malays as SOE managers

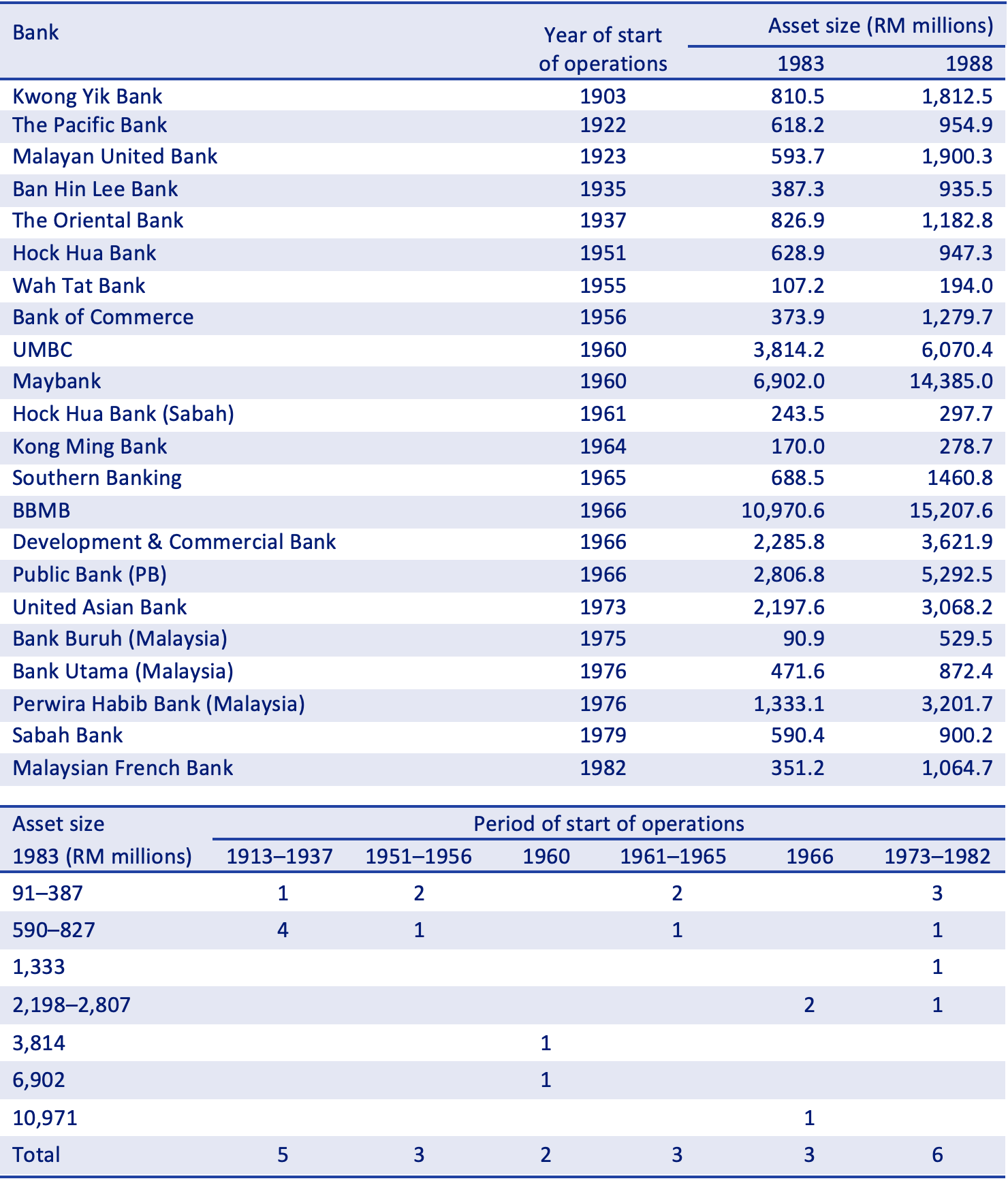

Before the NEP, banks were almost exclusively owned and operated by foreign or Malaysian-Chinese interests. The government established Bank Bumiputra Malaysia (BBMB) in 1965—in response to a resolution passed at the First Bumiputera Economic Congress of that year—aiming to spearhead Malay entry into banking and increase Malay participation in the country’s economy. Because of a bank run on Malayan Banking (Maybank) in 1966, owing to mismanagement and rifts between its major shareholders, the government took over control from its founder Khoo Teck Puat in 1966, retaining control

(Choi, 2014).

The NEP period

Malay entry into industry and commerce

Pernas had another role—pioneering the takeover of, or accumulation of sizeable stakes in, foreign-owned tin mines and plantations. It was the trailblazer for Permodalan Nasional Bhd, which in 1981 mounted a ‘Dawn Raid’ on Guthrie and Company (see below). The government authorized Permodalan Nasional Bhd to use its shareholdings in the acquired companies as the underlying shares to float unit trust funds to mobilize Malay savings on a massive scale from 1981. This authorization continued a trend. From the mid-1970s, Malay business groups, chambers, and associations had been pressing the government to divest profitable assets at cost to their members—firmly voiced during the Third Bumiputera Economic Congress in June 1980 (Jesudason, 1989; Thillainathan and Cheong, 2024).

At the state level, many State Economic Development Corporations (SEDCs) ventured into industry or commerce between 1971 and 1985, but most failed dismally despite receiving sizeable federal development allocations (Jesudason, 1989; Gomez, and Jomo 1997; Jomo and Wee, 2004). A few, such as the Selangor SEDC, which went into property development, and the Johor SEDC, which ventured into plantations and health care, were, however, successful.

Political parties, too, went into business. For the ruling United Malays National Organisation (UMNO), promoting entry of Malays into business was a secondary consideration—the main one was to raise money to help it retain power. The country’s first prime minister, Tunku Abdul Rahman, did this in 1961 by persuading friendly individuals to take over Utusan Melayu Press, the publisher of the leading Malay-language newspaper, and an important propaganda weapon3. Under the second prime minister, Tun Abdul Razak, reducing UMNO’s reliance on the Malayan Chinese Association—its coalition partner—as a source of funds was also a priority, as was heeding UMNO Youth’s demand to acquire the Malaysian operations of the Singapore-based Straits Times Press. The shares in the restructured New Straits Times Press (Malaysia) (NSTP) were bought in 1972 and held under a new vehicle, Fleet Holdings (by then with only informal links to UMNO).

Fleet Holdings spread its wings under the country’s fourth prime minister, Dr Mahathir, and from 1984 under Daim Zainuddin, UMNO’s treasurer (see below). In 1982, it became a controlling shareholder of another public limited company, hotel and property group Faber Merlin Malaysia (Searle, 1999). In 1986, it acquired Commerce International Merchant Bankers (CIMB); and the following year it took up significant interests in a string of other public limited companies and public listed companies (PLCs). With its aggressive growth, including the development of the Putra World Trade Centre (which included UMNO’s party headquarters), Fleet Holdings became highly leveraged.

To service Fleet Holdings’ mounting debt burden in a high interest rate environment, UMNO used its state powers to award companies under its control, or that of its nominees, a concession to operate a television channel and a major toll road—namely TV3 and the North–South Expressway—on favourable terms (Gomez, 1990; Wain, 2012). The award of the toll road concession was challenged on the grounds that it was conflicted4, but Malaysia’s Supreme Court dismissed the challenge on 15 July 1988 (Searle, 1999).

But, starting from April 1990, UMNO’s businesses were restructured to minimize political fallout from continuing controversies. The outcome involved the takeover of the toll road concession and the banking and insurance business by Halim Saad under Renong. Roxy Electric Industries, which had been renamed Technology Resources Industries, was taken over by Tajuddin Ramli, a Malay owner-manager. In January 1993, Renong sold its controlling stakes in media companies NSTP and TV3 to Realmild Sendirian Berhad, controlled by four NSTP executives, for RM800 million in a management buyout (Searle, 1999).

UMNO’s entry into business led to challenges and divestments, with politically connected Malay managers taking over the concessions as the new owner-operators, as with toll operator PLUS and the leading national telecommunications company CELCOM, or conducting a management buyout, as with NSTP and TV3. For PLUS, about 50 per cent of the North–South Expressway had been handed to it by the Malaysian Highway Authority at the start of its operations in 1994. It enjoyed a guaranteed minimum traffic volume, a substantial long-dated loan at below market interest rate, and a long holiday period on repayments (Thillainathan, 2021).

Malay owner-managers pre-1985

Pre-1985, Malaysia produced at least four dominant Malay owner-managers (see just below). Some others who became influential owner-managers post-1985 started out around the first half of the 1980s, such as Azman Hashim, Halim Saad, Rashid Hussain, Syed Mokhtar, and Tajuddin Ramli.

Syed Kechik Syed Mohamed

A confidante of Tun Mustapha, Chief Minister of Sabah, Founding Director of Sabah Foundation5, and Chairman of Sabah Land development Board, Syed Kechik enjoyed a meteoric rise in Sabah from the mid-1960s to the mid-1970s as he built a fortune from the extraction of timber from the 270 square miles of land allocated to three companies in which he had an interest, and from property development by the company he and his partners owned, to which large tracts of land had been alienated by the state. In 1976, Syed Kechik was, however, forced to take up residence in Kuala Lumpur when his patron was

displaced as Chief Minister of Sabah.

In Kuala Lumpur he continued to focus on property development and invest in real estate but also ventured into banking. In 1978, he acquired a 30 per cent interest in Development & Commercial Bank. His attempt in the early 1980s to wrest majority control of the Bank failed because he could not obtain the required regulatory approval (Searle, 1999). He also lost out to the Fleet Group in his bid for the TV3 licence, and failed to obtain approval for a huge property development by Sri Hartamas in Kuala Lumpur. ‘With assets reported to be worth RM800 million, Syed Kechik then appeared to represent the beginnings of a new class of independent Malay entrepreneurs.’ However, he was ‘increasingly marginalized from the new centres of power’ (Searle, 1999, pp. 134–135). With over-exposure to the property sector and the share market, and his failure to secure the required government approvals—lacking the political patronage he enjoyed during his phenomenal rise in Sabah—he failed to survive the mid-1980s’ economic crisis, which was accompanied by a collapse in property and share prices.

Ibrahim Mohamed

Ibrahim Mohamed was an owner-manager who scaled the heights of corporate Malaysia. During the 1970s, Ibrahim had built a powerful network of relationships with top politicians and business leaders. He helmed, jointly with Singaporean Brian Chang, the flagship Promet Bhd. It recorded a meteoric trajectory ‘whose profits trebled in 3 years, from RM41 million in 1981 to RM115 million in 1983, by which time it was the 14th largest company on the Kuala Lumpur Stock Exchange with a market capitalization exceeding RM100 million … but by 1985 it made a loss of RM92 million, while the company’s stock fell from RM11 a share in late 1981 to 80 sen a share in 1986, and its indebtedness to 18 banks soared to over RM100 million’ (Searle, 1999, pp. 157–159). In February 1986, he lost a corporate tussle with his partner when the banks forced his removal from the company. in November 1986 they placed the company in receivership and froze its assets.

In 1976, Ibrahim succeeded in acquiring a PLC, General Ceramics, and sold it in 1977 to its Chinese managing director who made it profitable. When he purchased a second but indebted PLC, Associated Plastics Industries (API) using his sale proceeds, it became a target of market speculation and its trading was suspended by the Kuala Lumpur Stock Exchange on suspicion ‘that API shares were being cornered by its directors’ (Searle, 1999, p. 156). Three years after Ibrahim’s Promet exit, he restructured API and renamed it Uniphoenix Corporation Bhd, but was unable to stem its losses. He exited the corporate world ‘when in August 1993 he pleaded guilty to selling 825,000 shares in … United Paper Holdings Bhd, he did not own and was fined RM500,000’ (Searle, 1999, p. 160).

Daim Zainuddin

Having achieved success as a property developer in Kuala Lumpur from the early 1970s, Daim Zainuddin was appointed chairman of Peremba—the commercial arm of the Urban Development Authority—to spearhead the entry of Malays as developers and owners of commercial properties in metropolitan areas. His most prominent development, with the Kuok group, was in Kuala Lumpur’s golden triangle, which includes the Shangri La hotel, as well as two office and apartment blocks. Daim also had oversight of UMNO companies from 1982 (Wain, 2012, p. 119). Daim had an exceptional capacity to carry out highly risky, lucrative deals, as illustrated by the way he handled the controlling stakes he exercised over UEP, the Subang Jaya developer, from December 1982 as well as UMBC, Malaysia’s third-largest bank, from 1984. He was then wearing a government and personal hat, and it was when the economy was slipping into the 1985–86 economic crisis.

UEP was ‘effectively controlled two-thirds’ by government-owned Peremba and Daim’s family company (Searle, 1999, p. 140). Around mid-1983, by injecting its Subang View hotel, UEP gained an 11 per cent stake in Faber Merlin, which a month earlier had come to be controlled by UMNO’s Fleet Holdings on terms which were deemed favourable to UEP. In January 1985, Daim and Peremba sold a 32 per cent stake in UEP in exchange for shares in Sime Darby. The latter firm’s minority shareholders were unhappy, as the run-up in UEP’s share price after Daim’s acquisition had made UEP’s share price higher than Sime Darby’s. The share swap gave Daim a 7 per cent stake in Sime Darby (Searle, 1999, p. 139).

Daim acquired his initial 41 per cent stake in UMBC from Multi-Purpose Holdings Bhd a week before he became finance minister in July 1984. He increased his stake to 50.3 per cent in June 1985 by buying the preferential rights issue that Pernas, the other joint controlling shareholder, chose to forgo. Daim managed to comply with a 1986 cabinet directive, requiring all ministers to divest their PLC shares, by selling his stake in its entirety to none other than Pernas in December 1986. ‘Bankers indicated that the sale enabled Daim’s family companies to realize a cash gain of almost RM100 million on their initial purchase of UMBC in 1984 through the share swap with Malaysia French Bank’ (Searle, 1999, p. 274).

Shamsuddin Abdul Kadir

Shamsuddin Abdul Kadir of Sapura Holdings was an owner-manager who was a success in manufacturing. He started his career in the Telecommunications Department of Malaysia in 1959 but joined the private sector in 1971. Sapura won virtual control of the domestic market by producing made-in-Malaysia telephones from 1977, entering into technology-transfer agreements with reputable foreign companies. It started off in 1975 by supplying, installing, and maintaining public payphones and by being one of the first local turnkey contractors to lay cables. In September 1984, Sapura acquired Malayan Cables, a PLC, to assure itself of cable supply to support its multimillion-ringgit cable-laying business and injected into Malayan Cables its principal operating company, ‘which had already begun to diversify its product range by the manufacture of public payphones, feature phones, PABXs [private automatic branch exchanges], main distribution frames and miniature protector connectors’ (Searle, 1999, p. 171).

With corporatization in 1987, as Syarikat Telekom Malaysia became more cost conscious, Sapura turned to manufacturing specialist telecommunications products to penetrate niche markets worldwide, either under licensing or on a joint-venture basis with the likes of GEC Plessey Telecommunications Ltd and Sumitomo. The Sapura Group had, by 1991, two PLCs in its stable, namely Uniphone Telecommunications Bhd and Sapura Telecommunications Bhd, and ‘the contribution of exports to company profits leapt from RM2 million in 1989 to RM170 million in 1993’ (Searle, 1999, p. 173).

Malay entry through takeover of plantations and tin mines

From the mid-1970s, the government started its aggressive programme to buy foreign-owned plantations and tin mines. It mounted a hostile takeover of Guthrie and Company, a large British-owned rubber and oil palm plantation conglomerate, on the London Stock Exchange in 1981, having earlier acquired a 30 per cent stake through Sime Darby—controlled by Pernas—after the latter narrowly failed in a takeover attempt of the company. The takeover was characterized as a ‘Dawn Raid’, even though it did not violate the Takeover Code of the United Kingdom (UK), although later there was a change in the takeover rules (Yacob and White, 2010). The purchases were at market prices and therefore did not constitute a ‘back-door’ nationalization.

In mining, Malaysia’s decision not to renew expiring British mining leases may have helped depress share prices of tin companies targeted for acquisition (Jesudason, 1989). From the late 1970s, the British-owned Chartered Consolidated and London Tin were gradually taken over by Pernas.

These acquisitions gave Malays a direct role in governing and managing plantations and tin mines, at a time when Malaysia was the world’s top producer of rubber and tin. The acquisition of plantations could not have been better timed, coinciding with a reversal in the terms of trade in favour of commodities (Young, Bussink, and Hassan 1980). With increasing competition from synthetic rubber and the higher international price of palm oil, many plantation managers switched from rubber to oil palm cultivation.

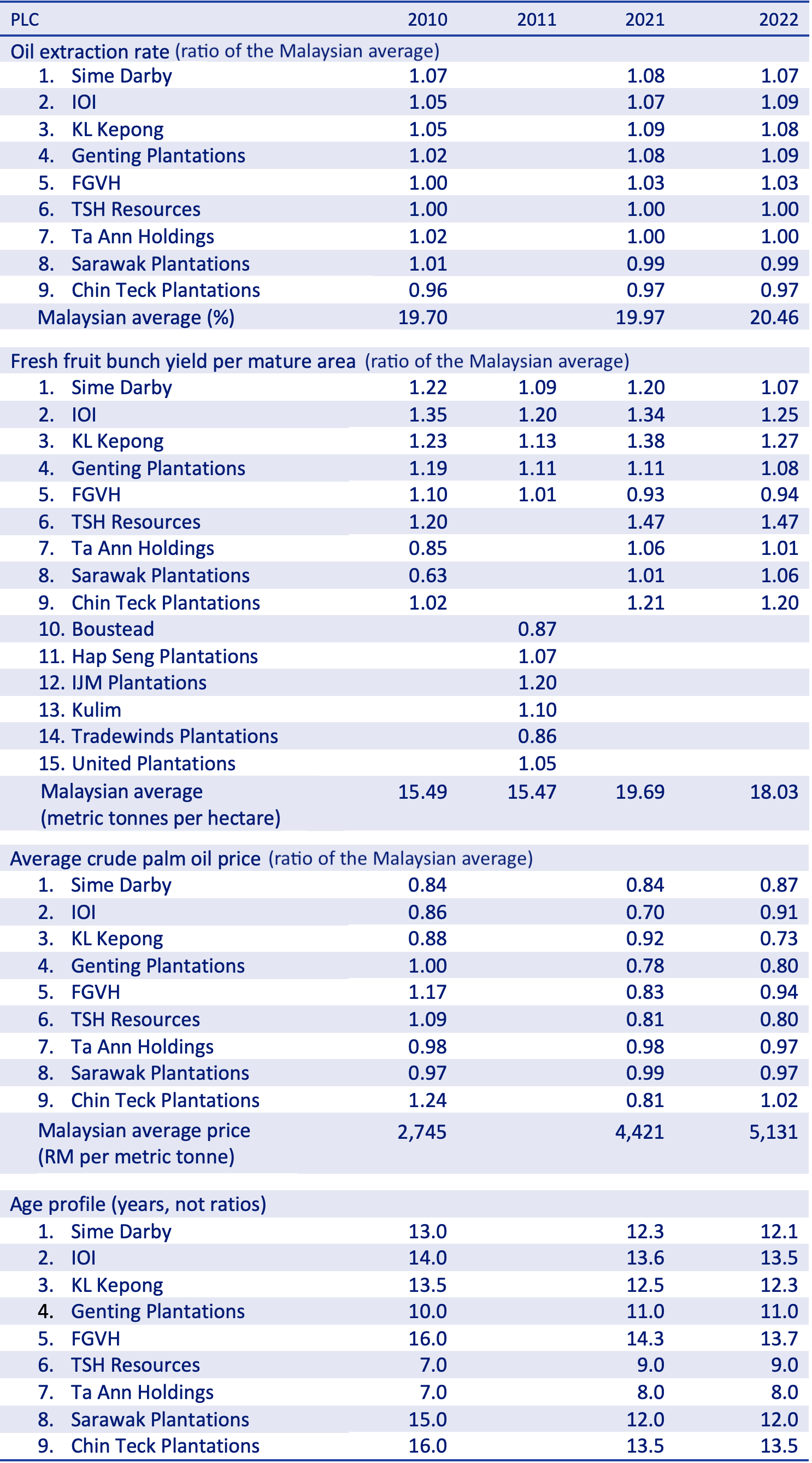

Malays emerged as dominant players in the plantation sector, owing to the massive FELDA-developed acreage and aggressive government takeovers of foreign-owned plantations, including of Guthrie and Company and of Harrisons and Crosfield, which were then, with Sime Darby, the three largest plantation companies by acreage owned (Low, 1985; Jesudason, 1989). Malay managers remained the dominant players in the plantation industry into the new millennium. Of Malaysia’s top 10 plantation companies, the market share of the three Malay-managed companies—Felda Global Ventures Holdings (FGVH), Sime Darby, and Tradewinds Plantations—was 14.8 per cent, whereas that of the seven non-Malay-managed companies was 12.5 per cent (FGVH, 2012, pp. 69–73).

Quantifying Malay entry into business

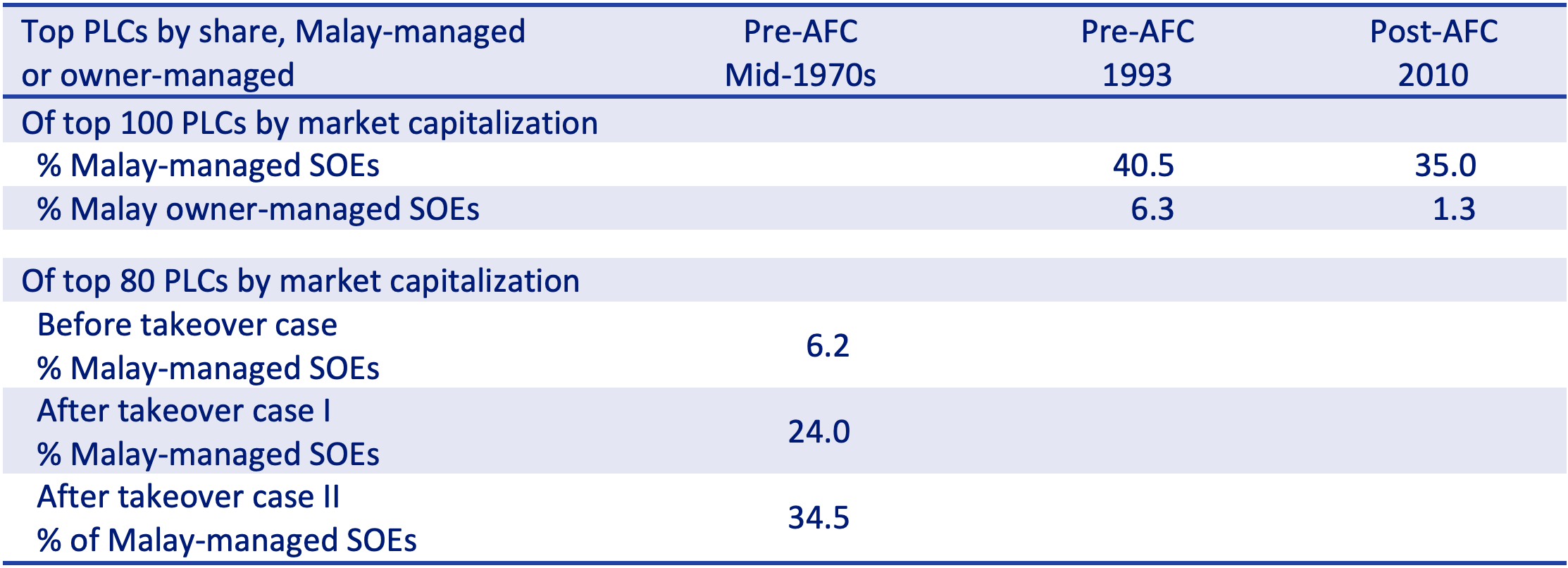

An attempt is made to quantify the size of Malay business entry, and what form it took, whether as manager or owner-manager. The available data are for the top 80 PLCs in 1974 by market capitalization (Tan, 1982; Perkins and Woo, 1998), and by the scale of operation for an entity that is not a PLC or a company. With the aggressive takeover of foreign-controlled PLCs—subsequently taken over by the Malaysian government by 1977—the share of listed Malay-managed SOEs shot up. Based on a lower threshold to identify the ultimate controlling shareholder, it rose to 24 per cent by 1977—excluding Singapore-controlled and -registered PLCs. The share of listed Malay-managed SOEs increases to 34.5 per cent if the estimate includes all UK-controlled plantation and mining PLCs that were taken over by Malaysian government interests by the mid-1980s (Table 1).

Table 1: Malay participation in PLCs as owner-manager or manager before and after the Asian Financial Crisis (AFC)

Performance of Malay-managed plantations

The disparity in the performance of Malay- versus Chinese-managed companies widened between 2010 and 2021–2022. During the pandemic, FGVH underperformed the Malaysian average by 6–7 per cent. Conversely, SDP’s outperformance of 7–20 per cent was significantly below that of IOI and KLK, which ranged between 25 and 38 per cent. The giant Malay-managed plantation PLCs are not performing as well as the Chinese-managed ones on yield. Even a business that enjoys increasing returns to scale (which is not the case with agriculture) can become too big to manage if it expands beyond a certain size, as is no doubt the case with FGVH and SDP. Further yields will be affected if replanting is slow. This is more likely to be the case with FGVH/Felda Group. Under its model, cash-constrained smallholders still play a significant role as co-owners. This is less so with the other major plantation groups. And FGVH/Felda Group, operating only in Malaysia, has also faced a more acute labour shortage.

Table 2: Performance of top PLCs as a ratio of the Malaysian average

Malay entry into banking via licensing and takeover, 1957–1998

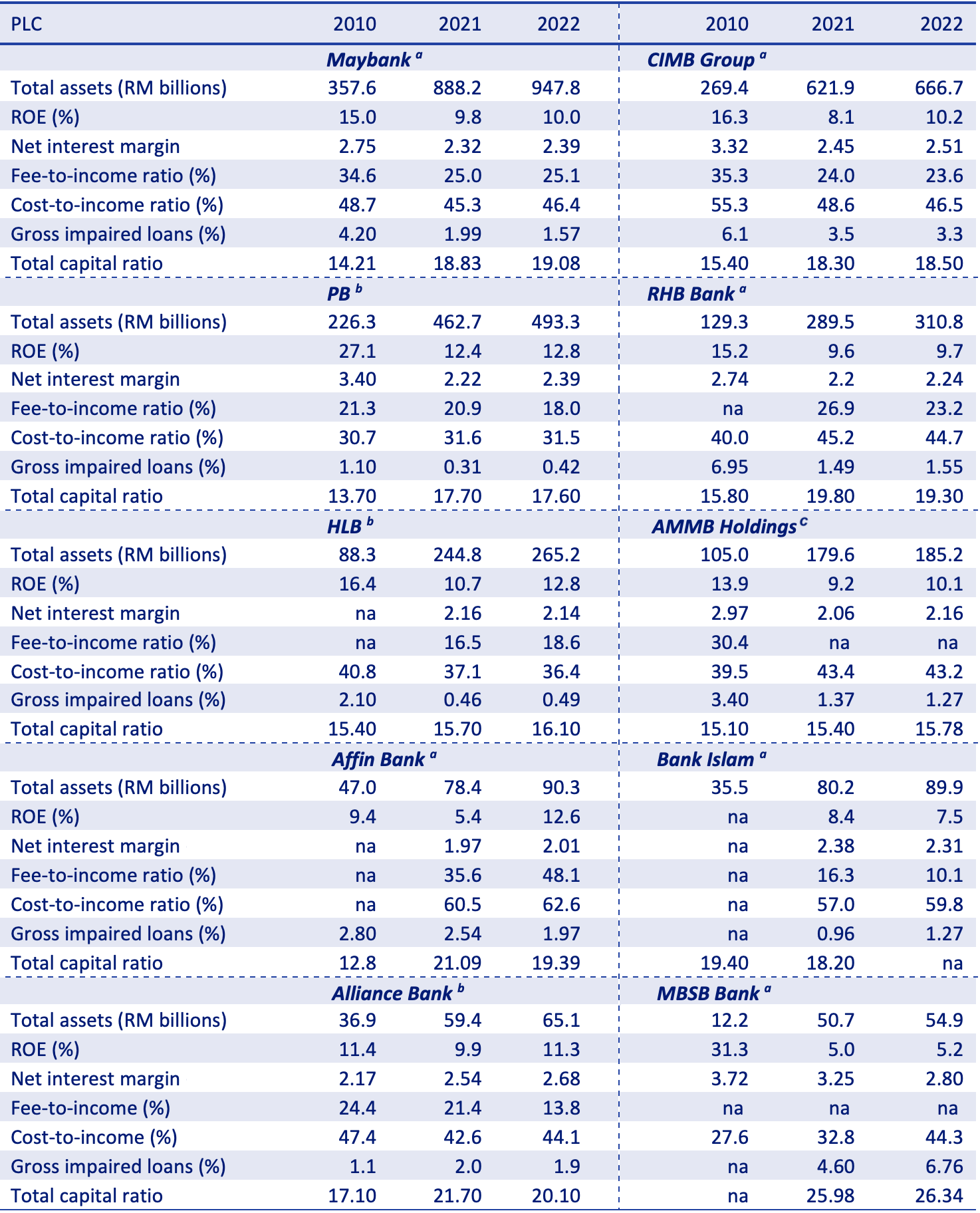

Performance of the banking sector

Concluding remarks

Bank Negara Malaysia [BNM], 1979, 1984, and 1989, Money and Banking in Malaysia. Kuala Lumpur: BNM.

Berle, A. and G. C. Means. 1932. The Modern Corporation and Private Property. New York: Harcourt, Brace and World, Inc.

Choi, S. H. 2014. I Remember, A Memoir. Singapore: Partridge Publishing.

Felda Global Ventures Holdings. [FGVH] 2012. Prospectus. Kuala Lumpur: FELDA.

Gomez, E. T. 1990. Politics in Business: UMNO’s Corporate Investments. Kuala Lumpur: Forum.

Gomez, E. T. and Jomo K. S. 1997, Malaysia’s political economy, Politics, patronage and profits, Cambridge: Cambridge University Press.

Hassan, B. W. 2012. Ownership and Control of Public Listed Companies in Malaysia: The Impact of the New Economic Policy. MSc Dissertation. University of Malaya.

International Monetary Fund [IMF], 2001. Malaysia: From Crisis to Recovery. Washington, DC: IMF.

Jesudason, J. V. 1989. Ethnicity and the Economy, The State, Chinese Business and Multinationals in Malaysia. Singapore: Oxford University Press.

Jomo, K. S. and Wee, C. H. 2004. Affirmative action and exclusion in Malaysia: ethnic and regional inequalities in a multicultural society. Background paper for the Human Development Report 2004.

La Porta, R., de Silanes, F.L., Shleifer, A., and Vishny, R. 1998. Law and Finance. Journal of Political Economy, 106(6), 1113–1155.

Lim, C. Y. 1967. Economic Development of Modern Malaya. Kuala Lumpur: Oxford University Press.

Lim, G. T. 2004. My Story. Subang Jaya: Pelanduk Publications.

Low, K. Y. 1985. The Political Economy of Corporate Restructuring in Malaysia A Study of State Policies with reference to Multinational Corporations. MSc Thesis. University of Malaya.

Permodalan Nasional Berhad. 2017. Annual Report. Kuala Lumpur: PNB

Perkins, D. H. and Woo, W. T. 1998. ‘Malaysia in Turmoil: Growth Prospects and Future Competitiveness’. University of California at Davis. https://faculty.econ.ucdavis.edu/faculty/woo/davosmal.html

Rajasingam, M. 2020. Navigating Turbulent Times. Petaling Jaya: Strategic Information and Research Development Centre.

Searle, P. 1999. The Riddle of Malaysian Capitalism, Rent-seekers of Real Capitalists? Honolulu: University of Hawaii Press.

Shakila Yacob, and White, N. J. 2010. ‘The “Unfinished Business” of Malaysia’s Decolonisation: The Origins of the Guthrie “Dawn Raid’’’, Modern Asian Studies, pp. 1–42.

Sieh Lee, M. L. (1982). Ownership and Control of Malaysian Manufacturing Corporations, Kuala Lumpur: University of Malaya Cooperative Bookshop Publications.

Tan, T. W. 1982. Income Distribution and Income Determination in West Malaysia. Kuala Lumpur: Oxford University Press.

Tate, M. 1989. Power Builds the Nation, Vol I: The Formative Years. Kuala Lumpur: Tenaga Nasional Berhad.

______ 1990. Power Builds the Nation, Vol II: Transition and Fulfilment. Kuala Lumpur: Tenanga Nasional Berhad.

Thillainathan, R. 1976. An Analysis of the Effects of Policies for the Redistribution of Income and Wealth in West Malaysia, 1957-1975. PhD Thesis. The London School of Economics.

______ 2021. Privatisation of toll roads to promote Malay entry into business: A critical review of distribution stance, returns, risk and Governance. Malaysian Journal of Economic Studies, 58 (1), pp. 145–174.

Thillainathan, R. and Cheong, K. C. 2024 (forthcoming). Malay Entry into Business and Scaling the Heights of Corporate Malaysia in the post-1985 period - An Assessment.

Wain, B. 2012. Malaysian Maverick: Mahathir Mohamad in Turbulent Times. 2nd Edition. Palgrave Macmillan.

Young, K., W. C. F. Bussink, and Hassan P. 1980. Malaysia: Growth and Equity in a Multi-Racial Society. Baltimore: John Hopkins Press.